Benchmark: Comparing the Monte Carlo Method with Nonparametric Bootstrapping

Ivan Jacob Agaloos Pesigan

2026-06-13

Source:vignettes/benchmark.Rmd

benchmark.RmdWe compare the Monte Carlo (MC) method with nonparametric bootstrapping (NB) for standardized regression coefficients. In this example, we use the data set and the model used in betaMC: Example Using the BetaMC Function.

library(betaMC)

library(boot)

library(microbenchmark)The BetaMC() function is used to generate MC confidence

intervals. The BetaNB() function is used to generate NB

confidence intervals.

BetaNB <- function(formula, data, B) {

statistic <- function(formula, data, indices) {

return(

coef(lm(formula = formula, data = as.data.frame(scale(data[indices, ]))))[-1]

)

}

return(boot.ci(boot(data = data, statistic = statistic, formula = formula, R = B)))

}Data and Model

df <- betaMC::nas1982Benchmark

Arguments

| Variables | Values | Notes |

|---|---|---|

| R | 5000 | Number of Monte Carlo replications. |

| B | 5000 | Number of bootstrap samples. |

benchmark <- microbenchmark(

MC = {

formula <- "QUALITY ~ NARTIC + PCTGRT + PCTSUPP"

object <- lm(formula = formula, data = df)

mc <- MC(object = object, R = R, type = "mvn")

BetaMC(object = mc)

},

NB = {

formula <- "QUALITY ~ NARTIC + PCTGRT + PCTSUPP"

object <- lm(formula = formula, data = df)

BetaNB(formula = formula, data = df, B = B)

},

times = 10

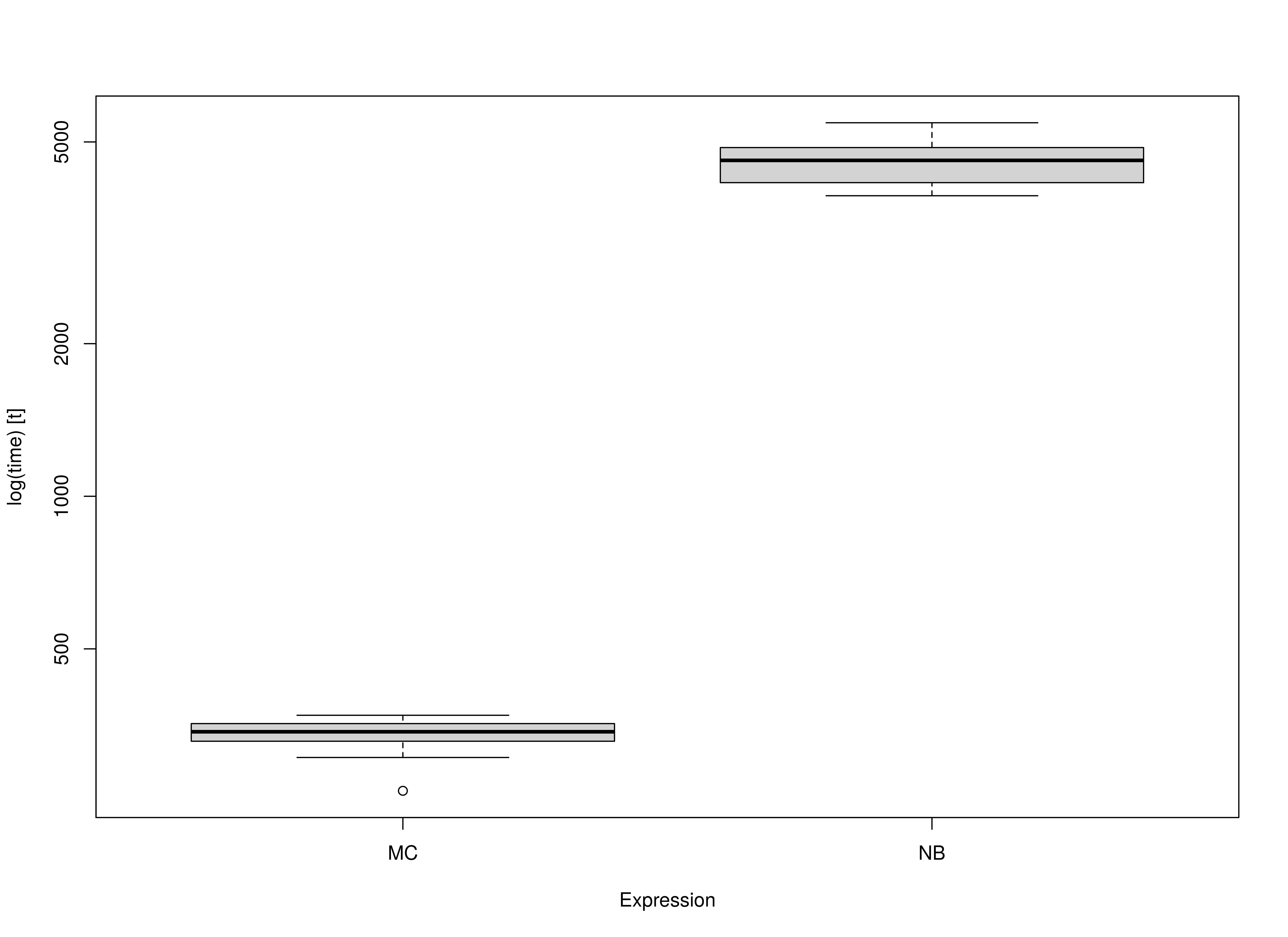

)Summary of Benchmark Results

summary(benchmark, unit = "ms")

#> expr min lq mean median uq max neval

#> 1 MC 323.0019 332.5833 342.8465 340.074 354.2382 368.3387 10

#> 2 NB 4726.7796 4756.0072 4813.2455 4765.061 4833.1233 5169.8796 10Summary of Benchmark Results Relative to the Faster Method

summary(benchmark, unit = "relative")

#> expr min lq mean median uq max neval

#> 1 MC 1.00000 1.0000 1.00000 1.00000 1.00000 1.00000 10

#> 2 NB 14.63391 14.3002 14.03907 14.01184 13.64371 14.03567 10