MCStd Function Use Case 4: Difference of Standardized Regression Coefficients in Multiple Groups

Ivan Jacob Agaloos Pesigan

2026-06-14

Source:vignettes/mcstd-4-difference-regression-coefficients-multigroup.Rmd

mcstd-4-difference-regression-coefficients-multigroup.RmdThe MCStd() function is used to generate Monte Carlo

confidence intervals for differences between standardized regression

coefficients in multiple groups.

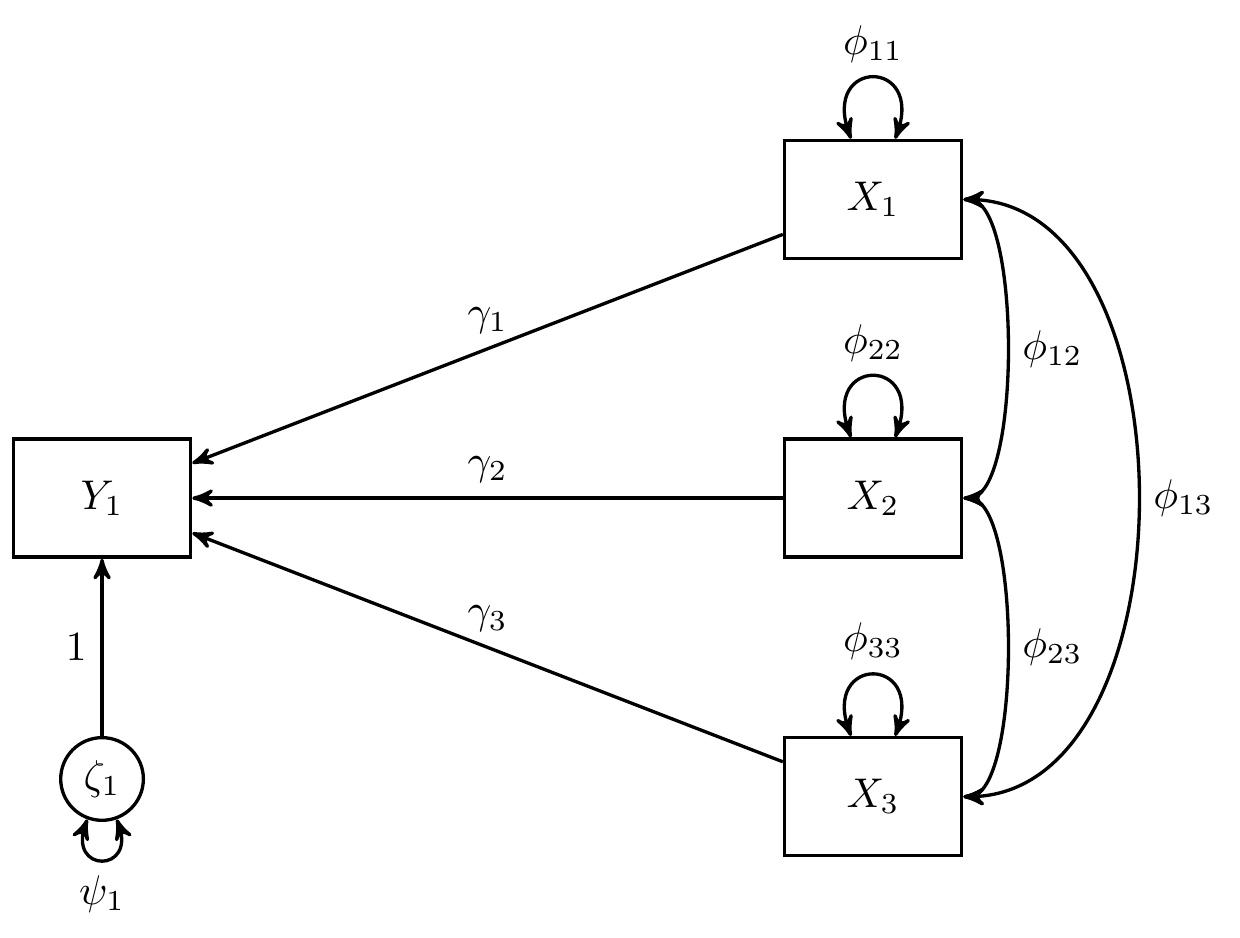

Data

In this example, we use data from Kwan & Chan (2014) with three groups (Hong Kong, Japan, and Korea) where child’s reading ability () is regressed on parental occupational status (), parental educational level (), and child’s home possession ()

Note that is the stochastic error term with expected value of zero and finite variance , is the intercept, and , , and are regression coefficients.

knitr::kable(

x = covs_hongkong, digits = 4,

caption = "Covariance Matrix for Hong Kong"

)| Y1 | X1 | X2 | X3 | |

|---|---|---|---|---|

| Y1 | 8176.0021 | 27.3990 | 28.2320 | 31.2722 |

| X1 | 27.3990 | 0.9451 | 0.6006 | 0.4326 |

| X2 | 28.2320 | 0.6006 | 0.7977 | 0.3779 |

| X3 | 31.2722 | 0.4326 | 0.3779 | 0.8956 |

nobs_hongkong

#> [1] 4625

knitr::kable(

x = covs_japan, digits = 4,

caption = "Covariance Matrix for Japan"

)| Y1 | X1 | X2 | X3 | |

|---|---|---|---|---|

| Y1 | 9666.8658 | 34.2501 | 35.2189 | 30.6472 |

| X1 | 34.2501 | 1.0453 | 0.6926 | 0.5027 |

| X2 | 35.2189 | 0.6926 | 1.0777 | 0.4524 |

| X3 | 30.6472 | 0.5027 | 0.4524 | 0.9583 |

nobs_japan

#> [1] 5943

knitr::kable(

x = covs_korea, digits = 4,

caption = "Covariance Matrix for Korea"

)| Y1 | X1 | X2 | X3 | |

|---|---|---|---|---|

| Y1 | 8187.6921 | 31.6266 | 37.3062 | 30.9021 |

| X1 | 31.6266 | 0.9271 | 0.6338 | 0.4088 |

| X2 | 37.3062 | 0.6338 | 1.0007 | 0.3902 |

| X3 | 30.9021 | 0.4088 | 0.3902 | 0.8031 |

nobs_korea

#> [1] 5151Model Specification

We regress Y1 on X1, X2, and

X3. We label the regression coefficient

for the three groups as gamma1.g1, gamma1.g2,

and gamma1.g3,

for the three groups as gamma2.g1, gamma2.g2,

and gamma2.g3, and

for the three groups as gamma3.g1, gamma3.g2,

and gamma3.g3.

model <- "

Y1 ~ c(gamma1.g1, gamma1.g2, gamma1.g3) * X1

Y1 ~ c(gamma2.g1, gamma2.g2, gamma2.g3) * X2

Y1 ~ c(gamma3.g1, gamma3.g2, gamma3.g3) * X3

gamma1.g12 := gamma1.g1 - gamma1.g2

gamma1.g13 := gamma1.g1 - gamma1.g3

gamma1.g23 := gamma1.g2 - gamma1.g3

gamma2.g12 := gamma2.g1 - gamma2.g2

gamma2.g13 := gamma2.g1 - gamma2.g3

gamma2.g23 := gamma2.g2 - gamma2.g3

gamma3.g12 := gamma3.g1 - gamma3.g2

gamma3.g13 := gamma3.g1 - gamma3.g3

gamma3.g23 := gamma3.g2 - gamma3.g3

"Model Fitting

We can now fit the model using the sem() function from

lavaan with mimic = "eqs" to ensure

compatibility with results from Kwan & Chan

(2011).

Note: We recommend setting

fixed.x = FALSEwhen generating standardized estimates and confidence intervals to model the variances and covariances of the exogenous observed variables if they are assumed to be random. Iffixed.x = TRUE, which is the default setting inlavaan,MC()will fix the variances and the covariances of the exogenous observed variables to the sample values.

Standardized Monte Carlo Confidence Intervals

Standardized Monte Carlo Confidence intervals can be generated by

passing the result of the MC() function to the

MCStd() function.

unstd <- MC(fit, R = 20000L, alpha = 0.05)

MCStd(unstd, alpha = 0.05)

#> Standardized Monte Carlo Confidence Intervals

#> est se R 2.5% 97.5%

#> gamma1.g1 0.0568 0.0191 20000 0.0194 0.0942

#> gamma2.g1 0.1985 0.0186 20000 0.1616 0.2353

#> gamma3.g1 0.2500 0.0150 20000 0.2208 0.2791

#> Y1~~Y1 0.8215 0.0103 20000 0.8004 0.8409

#> X1~~X1 1.0000 0.0000 20000 1.0000 1.0000

#> X1~~X2 0.6917 0.0076 20000 0.6766 0.7064

#> X1~~X3 0.4702 0.0115 20000 0.4474 0.4923

#> X2~~X2 1.0000 0.0000 20000 1.0000 1.0000

#> X2~~X3 0.4471 0.0117 20000 0.4237 0.4699

#> X3~~X3 1.0000 0.0000 20000 1.0000 1.0000

#> gamma1.g2 0.1390 0.0164 20000 0.1068 0.1711

#> gamma2.g2 0.1792 0.0158 20000 0.1480 0.2098

#> gamma3.g2 0.1688 0.0139 20000 0.1416 0.1961

#> Y1~~Y1.g2 0.8371 0.0088 20000 0.8196 0.8539

#> X1~~X1.g2 1.0000 0.0000 20000 1.0000 1.0000

#> X1~~X2.g2 0.6525 0.0074 20000 0.6380 0.6670

#> X1~~X3.g2 0.5023 0.0096 20000 0.4833 0.5208

#> X2~~X2.g2 1.0000 0.0000 20000 1.0000 1.0000

#> X2~~X3.g2 0.4452 0.0104 20000 0.4249 0.4651

#> X3~~X3.g2 1.0000 0.0000 20000 1.0000 1.0000

#> gamma1.g3 0.0863 0.0170 20000 0.0527 0.1193

#> gamma2.g3 0.2557 0.0164 20000 0.2236 0.2877

#> gamma3.g3 0.2289 0.0139 20000 0.2017 0.2563

#> Y1~~Y1.g3 0.7761 0.0103 20000 0.7556 0.7958

#> X1~~X1.g3 1.0000 0.0000 20000 1.0000 1.0000

#> X1~~X2.g3 0.6580 0.0079 20000 0.6425 0.6734

#> X1~~X3.g3 0.4738 0.0107 20000 0.4526 0.4945

#> X2~~X2.g3 1.0000 0.0000 20000 1.0000 1.0000

#> X2~~X3.g3 0.4353 0.0112 20000 0.4133 0.4570

#> X3~~X3.g3 1.0000 0.0000 20000 1.0000 1.0000

#> gamma1.g12 -0.0821 0.0251 20000 -0.1311 -0.0336

#> gamma1.g13 -0.0294 0.0257 20000 -0.0802 0.0208

#> gamma1.g23 0.0527 0.0236 20000 0.0070 0.0993

#> gamma2.g12 0.0193 0.0244 20000 -0.0286 0.0674

#> gamma2.g13 -0.0572 0.0248 20000 -0.1059 -0.0081

#> gamma2.g23 -0.0765 0.0228 20000 -0.1213 -0.0320

#> gamma3.g12 0.0811 0.0203 20000 0.0411 0.1209

#> gamma3.g13 0.0211 0.0204 20000 -0.0191 0.0613

#> gamma3.g23 -0.0601 0.0196 20000 -0.0988 -0.0217